Nvidia Earnings Report 2025 has once again captured the world’s attention. Every quarter, the company’s earnings become a global event — far more than a routine corporate update. Why? Because NVIDIA today is the backbone of the global AI revolution, and its financial performance reveals whether the AI boom is accelerating, stabilizing, or beginning to slow down.

As the company prepares to release its latest Q3 FY2026 earnings, investors, analysts, businesses, and even governments are watching closely. The stakes have never been higher. With AI spending reaching historic levels and enterprises racing to deploy generative-AI infrastructure, NVIDIA’s performance will act as a pulse check for the entire technology sector.

In this long-form deep-dive, we break down everything you need to know — the latest news, market expectations, analyst reactions, risks, opportunities, and what this means for the future of AI.

Why NVIDIA’s Earnings Matter So Much Right Now

The Evolution of NVIDIA: From Graphics Giant to the Core Engine of Global AI Infrastructure

NVIDIA has undergone a profound and strategic metamorphosis, fundamentally redefining its role in the global technology landscape. It is no longer accurately described as merely a Graphics Processing Unit (GPU) manufacturer. Over the past half-decade, the company has masterfully reinvented itself to become the world’s singular most dominant and influential provider of Artificial Intelligence (AI) infrastructure.

This transformation means NVIDIA’s specialized hardware and proprietary software ecosystem now serve as the foundational, non-negotiable plumbing for virtually every advanced technological domain.

The Unrivaled Reach of NVIDIA’s Architecture

The company’s high-performance silicon chips and interconnected platforms are the essential, high-octane fuel powering the critical engines of modern technology. Its pervasive technology underpins a comprehensive array of groundbreaking applications:

- Generative AI Models: NVIDIA GPUs form the massive compute clusters required to train and run large-scale models like GPT, Llama, and diffusion models that power everything from coding assistants to art generation.

- Cloud Data Centers: Hyperscalers (the major cloud providers) rely heavily on NVIDIA to offer their customers AI-as-a-service, making their data centers the primary factories for advanced computing.

- Robotics and Automation: The chips provide the “brains” for industrial robots, drones, and autonomous machinery, enabling them to perceive, reason, and act in complex, real-world environments.

- Autonomous Driving: The NVIDIA DRIVE platform is a specialized, end-to-end solution for training, testing, and operating the self-driving systems used by automotive manufacturers and robotaxi fleets.

- Scientific Simulations: From climate modeling to drug discovery and astrophysics, researchers use NVIDIA’s accelerated computing to run complex, long-duration simulations exponentially faster than traditional CPUs.

- Digital Twin Platforms (Omniverse): Its platforms facilitate the creation of highly accurate, real-time virtual representations of physical systems, factories, and entire cities, used for design, collaboration, and training.

- High-Performance Computing (HPC) for Enterprises: Corporations across finance, energy, and manufacturing leverage these supercomputing-level capabilities to solve incredibly difficult computational problems, driving new levels of operational efficiency.

More Than Just a Financial Report: A Global AI Indicator

Given this unparalleled market penetration, an NVIDIA earnings announcement transcends a typical corporate financial report. It has become a global economic barometer and a leading indicator of AI investment.

When technology behemoths such as Microsoft, Google, Amazon, Meta, Tesla, OpenAI, and thousands of venture-backed startups commit to scaling their AI strategies, they must, by necessity, purchase NVIDIA’s hardware. This immediate and massive demand directly translates into revenue and profit for the company. Conversely, any slowdown or pause in capital expenditure by these giants is instantaneously felt within NVIDIA’s sales figures and future guidance.

This symbiotic relationship explains why global stock markets—from the financial hubs of Wall Street and the City of London to the technology exchanges across Asia—respond with such acute volatility to the company’s quarterly results. NVIDIA’s performance is no longer viewed in isolation; it is widely understood to represent the pulse, or the very heartbeat, of the rapidly expanding AI economy.

Latest News: What’s Happening Ahead of NVIDIA’s Earnings

Here are the most important recent developments surrounding NVIDIA’s upcoming earnings:

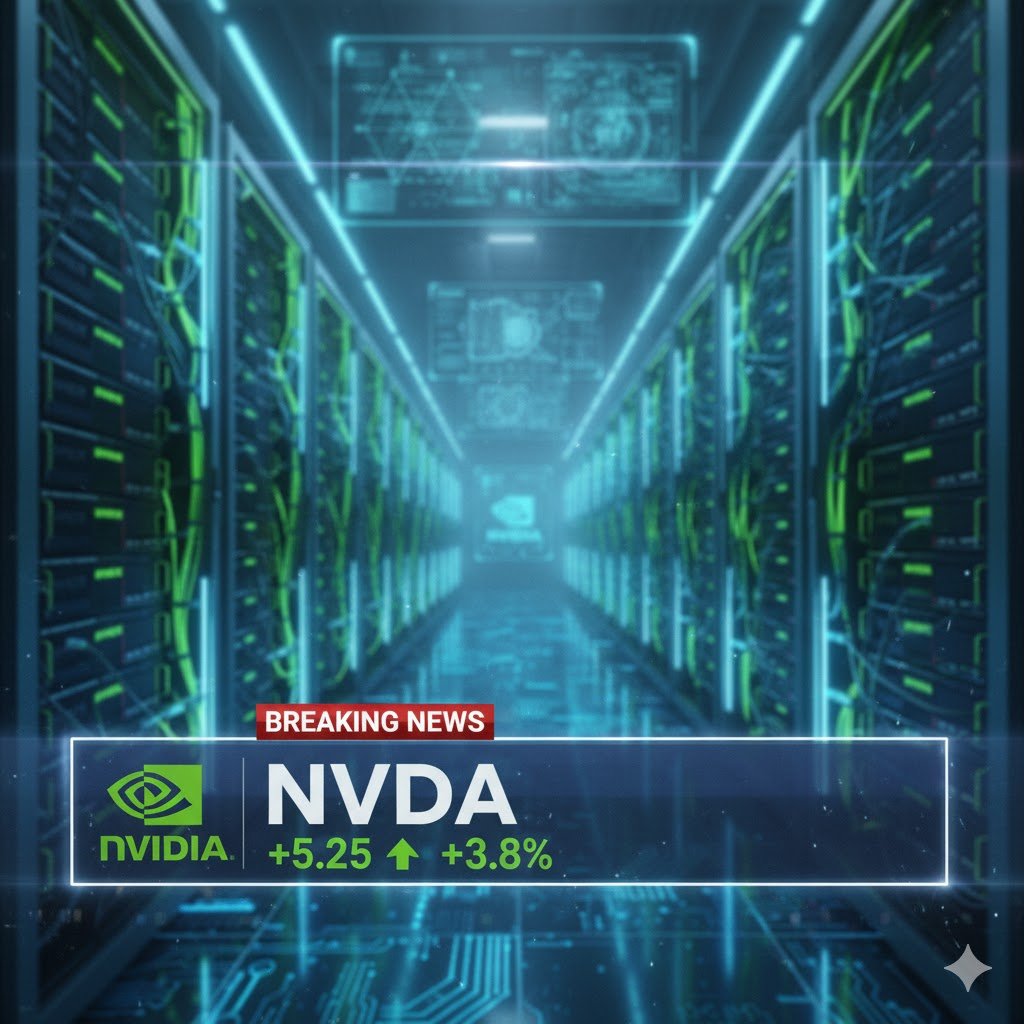

Revenue Expected to Hit Nearly $55 Billion for the Quarter

Analysts are expecting blockbuster results again, predicting:

- Revenue: ~$54.9 billion

- EPS: ~$1.25

- Data center revenue: ~$49 billion

The data-center segment — driven by AI training, inference, and enterprise deployment — continues to dominate NVIDIA’s business model.

High Volatility Expected: A Possible $300 Billion Stock Swing

Market analysts and options traders expect NVIDIA’s stock to be extremely volatile post-earnings.

Options data suggests NVIDIA could move ±7% after the report — which equals a potential $300+ billion market cap swing.

A single earnings call could change the value of the company by an amount larger than the GDP of some countries.

Is the AI Boom Slowing or Accelerating?

A major question economists and investors are debating:

Are we in an AI bubble? Or is this still the early stage of a historic tech revolution?

Key factors behind this debate include:

- Whether enterprises will sustain massive AI spending

- How quickly cloud providers can scale AI systems

- Whether generative AI monetization is profitable enough

- Concerns around valuation and market over-excitement

NVIDIA’s earnings will play a central role in answering these questions.

Big Investors Are Making Bold Moves

One notable piece of news:

Peter Thiel’s hedge fund recently sold off its entire NVIDIA stake.

This doesn’t necessarily reflect poor company performance — many investors are simply locking in profits after historic NVIDIA gains.

But this move has definitely triggered conversations about whether investors believe NVIDIA still has room for another big run.

NVIDIA’s Shift to Smartphone-Style Memory Could Double Server Memory Prices

One of the most interesting developments is NVIDIA’s decision to adopt LPDDR-based AI server memory — technology commonly found in smartphones.

Why this matters:

- Lower power consumption

- More efficient data throughput

- But global supply is limited

Analysts predict this change could cause server-memory prices to double by late 2026, potentially increasing AI infrastructure costs across the industry.

What Analysts Expect from the Earnings Call

Financial analysts are highly focused on several key areas:

Strength of the Data Centre Segment

This is NVIDIA’s most important revenue driver.

Analysts expect continued explosive demand for:

- H200 GPUs

- Blackwell (B100, B200) architecture

- High-bandwidth memory (HBM)

- NVIDIA DGX and enterprise AI servers

- Networking and InfiniBand solutions

If this segment performs strongly, NVIDIA’s stock may jump post-earnings.

Forward Guidance Will Matter More Than Actual Results

Even if NVIDIA beats current expectations, the most important part will be:

How strong is the company’s guidance for the next quarter and fiscal year?

Because the market has priced in extremely high expectations, NVIDIA must show:

- AI demand is still accelerating

- Cloud hyperscalers are continuing massive AI infrastructure spending

- Enterprise AI adoption is growing

- No major slowdown in chip shipments

A strong “beat and raise” could spark another surge in tech stocks.

China Restrictions & Geopolitical Risk

Export controls continue to affect how NVIDIA sells AI chips into China.

While NVIDIA has created alternatives for that market, uncertainty remains.

Investors will want clarity on:

- How much of China demand is still intact

- Whether new U.S. restrictions might come

- How NVIDIA plans to offset potential losses

Margins & Supply-Chain Constraints

High-bandwidth memory (HBM) supplies remain extremely tight.

NVIDIA needs to address:

- Component shortages

- Manufacturing capacity

- Memory supply issues

- Cooperation with partners like TSMC & Samsung

Margins could fluctuate based on these factors.

Market Sentiment: Optimism Mixed With Caution

Investors, analysts, and media seem split into two camps:

The Bullish View: “NVIDIA Will Keep Winning”

Supporters argue:

- AI spending is still in early stages

- Enterprises are just beginning gen-AI deployment

- NVIDIA has unmatched technological leadership

- Product pipeline (Blackwell, Rubin, AI networking) is extremely strong

- Hyperscalers already have multi-year GPU orders

Many analysts believe NVIDIA will beat expectations again.

The Bearish View: “Valuations Are Too High”

Others warn:

- The stock price already reflects massive future growth

- Any slowdown—even slightly—could trigger a sharp correction

- Competition from AMD, Intel, and custom AI chips is rising

- Memory and chip constraints pose risks

- Macro-economic uncertainty could hit tech investment

This tension creates volatility around earnings.

The Bigger Picture: What NVIDIA’s Results Will Mean for the AI Industry

NVIDIA’s performance will shape more than its own stock — it will influence:

- AI startups valuation

- Cloud provider cap-ex strategy

- Semiconductor sector performance

- AI model development speed

- Availability of GPUs globally

- Enterprise adoption rates

Here are the broader implications:

If NVIDIA Beats Expectations

- Massive confidence boost in AI sector

- Tech stocks likely surge

- Increased AI spending from global enterprises

- Positive signal for companies like AMD, TSMC, ASML, Supermicro

- Accelerated GPU investments across Big Tech

If NVIDIA Misses Expectations

- AI stock correction possible

- Analysts may rethink the pace of AI investment

- GPU-dependent companies may fall

- Tech market volatility increases

Because NVIDIA is the “AI barometer,” any weakness could ripple throughout global markets.

The Future: What Comes After This Earnings Cycle

Here’s what to expect from NVIDIA over the next several years:

NVIDIA’s Strategic Roadmap: The Three Pillars of Future AI Dominance

NVIDIA is meticulously planning its dominance not just for the current year, but for the entire back half of the decade. Its strategy is anchored by a trifecta of innovation: relentlessly advancing its core hardware architecture, aggressively monetizing its software ecosystem, and pioneering the next wave of ‘Physical AI’ applications.

Generational Hardware Acceleration: The Chip Roadmap

NVIDIA adheres to a rapid, roughly two-year cadence for launching its flagship data center architectures, and the immediate future is defined by two major leaps in computational power.

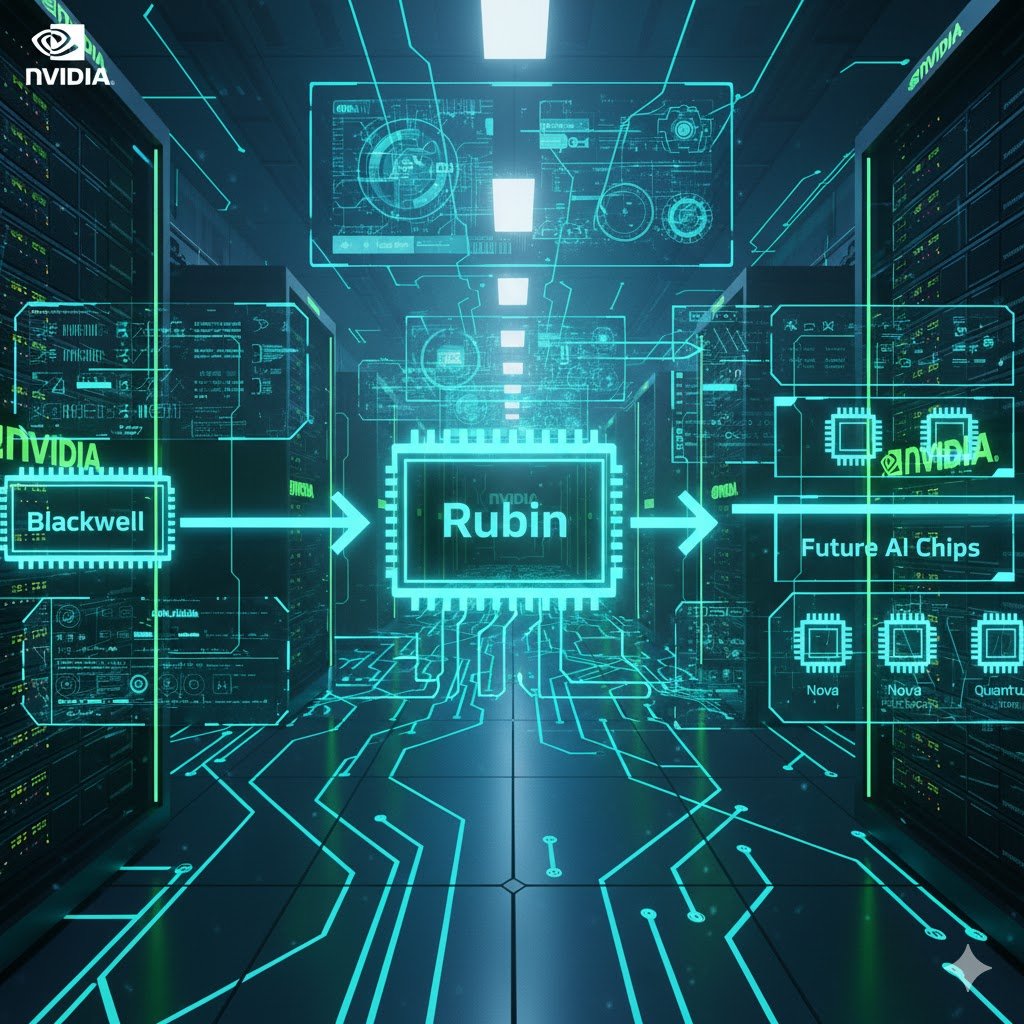

6.1 The “Blackwell” Architecture Rollout (2024–2025)

This generation, already entering mass deployment, represents a monumental engineering effort. Blackwell is a key answer to the escalating demands of training and deploying massive Generative AI models (like Large Language Models and diffusion models). Key features include:

- Massive Transistor Count and Design: It features GPUs constructed from multiple interconnected dies (chiplets) on a single package, packing over 200 billion transistors.

- Next-Gen Interconnect: The architecture significantly enhances the proprietary NVLink interconnect, allowing unprecedented speed and bandwidth (e.g., up to $1.8 \text{ TB/s}$ per GPU) to link hundreds of GPUs into a single, cohesive supercomputer (e.g., the GB200 NVL72 system), crucial for handling trillion-parameter models.

- Transformer Engine V2: It introduces new precision formats and optimizations specifically tailored for the Transformer architecture, dramatically improving both the speed of training (the time it takes to create a model) and the efficiency of inference (the time it takes to run the model). This drives massive demand from hyperscalers like Amazon, Google, and Microsoft.

The “Rubin” Architecture (2026)

Following Blackwell, the Rubin architecture (and the integrated Vera CPU/Rubin GPU platform) is expected to deliver the next dramatic generational leap, likely in 2026. This launch is highly anticipated for its technological breakthroughs:

- Process Node Shrink: Rubin is projected to leverage an even more advanced manufacturing process, such as TSMC’s 3 nm process, which inherently increases efficiency and transistor density.

- Memory Innovation (HBM4): It is expected to debut High Bandwidth Memory (HBM) version 4, which will significantly boost both the capacity and bandwidth of on-chip memory—a critical bottleneck for the largest AI models.

- Performance Targets: Industry projections suggest Rubin will aim for multiple times the performance of Blackwell (e.g., a 50 petaflops boost in FP4 performance per GPU), signaling NVIDIA’s commitment to an aggressive roadmap designed to outpace any competition.

Expansion into High-Margin AI Software Platforms

NVIDIA’s dominance is increasingly cemented by its software moat—the proprietary and expansive ecosystem built atop its hardware. These platforms are transitioning from being mere “tools” to becoming potential massive future revenue sources through enterprise licensing, subscription services, and developer adoption.

- NVIDIA Omniverse: This is a platform for building and operating digital twins and industrial metaverse applications. It is used for large-scale, physically accurate simulations—from designing entire factories to training autonomous vehicles. Omniverse’s value comes from allowing companies to simulate the physical world before deployment, saving billions in real-world costs.

- NeMo (LLM Development Framework): This is a comprehensive, cloud-native framework designed to help enterprises build, customize, and deploy their own specialized Generative AI models. By providing pre-trained models, optimization tools, and security features, NeMo transforms AI from a custom research project into a scalable enterprise solution.

- CUDA Advancements and Enterprise AI Frameworks (NVIDIA AI Enterprise): CUDA is the parallel computing platform that locks developers into the NVIDIA ecosystem. It’s continually updated with new libraries (CUDA-X) and specialized AI microservices (like NVIDIA NIM) that simplify and accelerate the deployment of trained models. The subscription-based NVIDIA AI Enterprise suite bundles this software for reliable, scalable deployment in corporate data centers, establishing a lucrative, recurring revenue stream on top of hardware sales.

AI-Powered Robotics, Autonomous Driving & Edge AI

These three areas represent new, multi-billion-dollar market opportunities that will drive the company’s growth beyond the cloud data center. They shift AI from the virtual world of servers to the physical world of machines.

- AI-Powered Robotics (Physical AI): The market for smart robots, including humanoid robots, is just beginning. NVIDIA is providing the underlying compute platform (Jetson) and the simulation environment (Omniverse) to train these “physical AI” systems, enabling them to safely learn skills in the virtual world before they operate in factories, warehouses, or homes.

- Autonomous Driving (DRIVE Platform): This is a complete, safety-certified stack for the automotive industry, covering everything from the powerful in-vehicle computer to the data center infrastructure needed for training the vehicle’s AI. As self-driving technology matures and scales globally, the volume and complexity of the embedded hardware needed will drive substantial long-term growth.

- Edge AI: This refers to placing AI processing power directly on devices—at the “edge” of the network—instead of in the cloud. Examples include smart cameras, industrial IoT, and medical devices. NVIDIA’s Jetson platform leads this space, catering to the growing need for real-time decision-making, low latency, and enhanced data privacy in applications where sending data back to a central cloud is impractical.

Final Thoughts: A Make-or-Break Moment for AI Markets

NVIDIA’s latest earnings report will influence:

- Where AI goes next

- How fast companies adopt generative AI

- How investors value tech companies

- How governments approach AI strategy

- Whether the AI boom accelerates — or cools off

As the world waits for NVIDIA’s results, one thing is clear:

This is not just another earnings report. It’s a global event shaping the future of AI.

If NVIDIA continues its explosive growth, the AI boom may just be getting started.

If not, it could mark the beginning of a new, more cautious era.

Either way, NVIDIA remains the company at the center of the technological revolution.

FAQs

NVIDIA’s Q3 FY2026 Earnings: The AI Industry’s Moment of Truth

NVIDIA is scheduled to report its financial performance for the third quarter of fiscal year 2026 (ending October 26, 2025) after the U.S. market closes today, Wednesday, November 19, 2025. Given the company’s position as the primary supplier for the global Artificial Intelligence boom, this event is far more than a corporate filing—it is widely considered a bellwether for the entire AI infrastructure investment cycle.

1. High Expectations: The Numbers to Watch

Analysts and investors have set an exceptionally high bar, demanding continued rapid growth to justify NVIDIA’s premium market valuation.

| Key Metric | Analyst Consensus Estimate | Significance and Context |

| Total Revenue | $\sim\text{US } \$54.8 \text{ billion}$ | This represents a massive $\sim55\%+\text{ Year-over-Year (YoY) increase}$. The market expects NVIDIA’s total sales to maintain a blistering pace, fueled almost entirely by demand from cloud providers and major tech firms building their AI compute clusters. |

| Adjusted Earnings Per Share (EPS) | $\sim\text{US } \$1.25$ | The expected EPS demonstrates the extraordinary profitability of NVIDIA’s specialized hardware. Stability in the high-seventies range for gross margins will be necessary to meet or exceed this target. |

| Data Center Revenue | $\sim\text{US } \$48 \text{ billion} \text{ – } \$49 \text{ billion}$ | This segment, driven by sales of its powerful GPUs and associated networking gear, is the core focus. It is expected to account for an unprecedented $\sim88\%$ to $90\%$ of total company revenue, showing the full depth of the AI pivot. |

The Crucial Subplots: Beyond the headline numbers, investors will be laser-focused on:

- Gross Margins: Confirmation that the company can sustain high-seventies percentage gross margins, proving its pricing power and operational efficiency in the face of rapidly scaling production.

- Blackwell Architecture Ramp: Updates on the successful mass production and delivery volumes of the latest-generation Blackwell chips, which are critical for driving revenue through the rest of 2026.

- China/Export Clarity: Management commentary regarding the ongoing impact of U.S. export restrictions on sales to China and how much new demand from non-restricted markets is offsetting this drag.

This is a comprehensive breakdown of the major financial and market talking points surrounding NVIDIA’s upcoming earnings. I will convert this into a detailed, human-written, and informative analysis, focusing on the context and implications of each point.

2. Earnings Release and Conference Call Timing

The results will be released during an active trading period, ensuring high volatility in the after-hours market.

| Event | Time (Approximate) | Notes |

| Results Release | After U.S. Market Close | The official financial report will be published after 4:00 p.m. Eastern Time (ET). |

| Earnings Conference Call | $\sim2:00 \text{ p.m. Pacific Time (PT)}$ | This typically begins shortly after the release, where CEO Jensen Huang and CFO Colette Kress provide crucial forward-looking guidance and address analyst questions. |

This is a comprehensive breakdown of the major financial and market talking points surrounding NVIDIA’s upcoming earnings. I will convert this into a detailed, human-written, and informative analysis, focusing on the context and implications of each point.

3. Investment Debate: Is NVDA Still a Strong Buy?

The high-flying stock presents a classic debate between unprecedented growth and a “priced-for-perfection” valuation.

The Bullish Thesis

Proponents argue that the stock is a “must-own” based on: Unrivaled AI Leadership (NVIDIA’s software/hardware ecosystem, anchored by CUDA, maintains an insurmountable competitive moat); Strong Growth Prospects (The multi-year AI infrastructure build-out by hyperscalers guarantees substantial future revenue); and a robust Next-Gen Pipeline (The successful ramp of Blackwell and the anticipation for the Rubin architecture keep the growth story intact).

The Cautionary Stance

Skeptics highlight significant risks: High Valuation (The stock trades at a premium that implies flawlessness, leaving little room for error); Slowing Sequential Growth (Any sign that quarter-over-quarter revenue growth is decelerating will be interpreted negatively); Supply-Chain & Export Risks (Geopolitical trade restrictions and potential bottlenecks in sourcing advanced memory/components remain constant threats).

Conclusion: The stock is considered a strong buy only for investors with high conviction in the long-term durability of AI hardware demand. Those cautious about the near-term economic environment or valuation risk may opt to wait for a clearer outlook or diversify.

Earnings Beat & Investor Sentiment

The market is currently in a state of nervous anticipation, with recent news adding to the volatility.

Did NVIDIA Beat Earnings? As the report is scheduled for release today, November 19, 2025, the actual results are not yet available. While NVIDIA has a strong historical track record of beating estimates, the consensus expectations are now so elevated that delivering a significant beat is harder than ever.

Peter Thiel’s Notable Exit: News that billionaire investor Peter Thiel’s hedge fund sold off its entire stake in NVIDIA (over 537,742 shares) during the previous quarter has generated significant market commentary. High-profile exits like this, even if driven by portfolio management rather than fundamental skepticism, can fuel concerns about AI valuations being stretched thin.

Stock Volatility: The period leading up to the report has seen high trading volumes and significant price swings, with the stock recently dipping (e.g., down 9$\sim8\%$ in recent weeks) amid broader market caution and AI valuation fears.10 The implied volatility from the options market suggests traders are expecting a 11$\pm7\%$ to 12$8\%$ price swing immediately following the announcement.